The key towards achieving inclusive financial growth is to make a strong effort to embed Fourth Industrial Revolution technologies, like Islamic fintech, to ensure fair and equitable distribution across income groups, and shared prosperity for all, in line with the recently-announced Malaysia Digital Economy Blueprint and Malaysia 5.0,” said MDEC chairman Datuk Wira Dr Hj Hussin Mohamed Ariff.

Malaysia’s excellent track record in fundraising augurs well overall, with the Securities Commission reporting a 130% increase in 2018, involving 1,449 SME (small and medium-sized enterprises), 18,700 investors (91% increase), and 5,612 campaigns (131% increase) launched.

The Islamic capital market grew by 8%, to RM2 trillion, outpacing overall capital market growth of 3%.

Bank Negara Malaysia (BNM) and the Securities Commission have allowed innovation in fintech to proliferate such expansion.

The government, through MDEC, have implemented various measures and initiatives. One such initiative is the Digital Financial Inclusion, which is aimed at improving the B40 (bottom 40% earners) and micro SME’s knowledge on financial services.

While FinTech Booster, in collaboration with BNM, is a capacity-boosting programme by MDEC to assist fintech companies, both local and international, to develop their products and services via three strategic modules: Legal and Compliance, Business Model and Technology.

MDEC Accelerates Plans to Attract High-Value Digital Global Business Services (GBS)

MSC Malaysia currently counts 579 active Global Business Services (GBS) companies within its fold, with 57% being foreign direct investments (FDIs). 30% of the foreign-owned GBS are part of the Forbes Global 2000 and Fortune 500 companies such as HSBC Electronic Data Processing (Malaysia) Sdn. Bhd., Jabil Global Business Services and Dassault Systèmes.

Although the number of active GBS companies accounts for approximately 20% of the total number of active MSC Malaysia companies, GBS is the largest contributor to MSC Malaysia’s performance, adding up to 50% of investments, 66% of exports, 61% of jobs created.

“Looking at the current GlobalData findings, the Business Process Management or what we term Global Business Services (GBS) market size in Malaysia is expected to grow from US$1.3bn in 2019 to US$1.5bn by the end of 2024. On that account, we are in a position of strength to bring more FDIs to this sector. The Government’s commitment to improving digital infrastructure and providing a pipeline of digitally-ready workforce allows us to reinvent ourselves as the preferred location for high-value GBS such as Robotic Process Automation (RPA) Analysis, Artificial Intelligence (AI) and Data-led processing and Cybersecurity.” - Raymond Siva, Senior Vice President, Investment and Brand, and Chief Marketing Officer (CMO) of Malaysia Digital Economy Corporation (MDEC).

“The role of digital technology and services is evident, especially following the outbreak of the COVID-19 pandemic which has led to further acceleration of digitalisation and accentuated GBS as a key pillar for an organisation’s resilience and agility. Many organisations are relying on GBS to help them explore and deliver innovation, automation, advanced services, and new ways of working. The scope of GBS now includes finance, information technology (IT), Human Resource (HR), and procurement, as well as other functions, and that can be delivered onshore or offshore,” added Siva.

“The trend is clear in Malaysia; companies are leveraging the GBS model to adopt and accelerate digital transformation, shifting focus from cost arbitrage to value-driven services,” Siva said.

While Finance, HR and Customer Experience are the most common services, intelligent automation and data analytics now feature among the top range of services. Value-add and cost-saving from streamlining and centralising core functions are major factors encouraging more and more companies to outsource their business activities.

“Malaysia is now home to nearly half of all analytics-based services in ASEAN. To accelerate this growth, MDEC is engaging the industry to listen to their needs, develop progressive and conducive policy and regulatory framework, and a robust pipeline of digital talents,” he added.

The Government’s support outlined in the Malaysia Digital Economy Blueprint (MyDIGITAL) through various phases until 2030 to drive the country’s high value-added economy and to become a net exporter of home-grown technologies and digital solutions will complement the rest of the national digital economy development initiatives such as the country’s GBS sector in the coming years.

Such moves will go a long way towards boosting investor confidence and for these companies to establish Malaysia as their preferred base to other emerging GBS locations such as India and China.

“MDEC will continue to lead the nation’s digital economy transformation towards the aspiration of Malaysia 5.0, enabling a society that is deeply integrated with Fourth Industrial Revolution (4IR) technology such as Internet of Things (IoT), Data Analytics, AI, and Blockchain. We have embarked on initiatives to empower more digitally-skilled Malaysians, enable digitally-powered businesses and attract more digital investments. In doing so, we are creating new opportunities for both the people and businesses, contributing to the growth of a sustainable and equitable digital economy, and firmly establishing Malaysia as the Heart of Digital ASEAN,” said Siva.

Fast Facts

Southeast Asia’s economy is among the fastest-growing in the world and is projected to be the fourth-largest regional economy by 2030. Analysts also expect this growth to boost the e-commerce market, with the digital economy set to grow from US$31 billion in 2015 to US$197 billion by 2025. Revenue from the e-commerce market in Southeast Asia in 2021 is expected to be US$67.6 billion, representing annual growth of 10.3%.

Vietnam Poised for Growth as Digital Tech Drives Another Industrial Revolution

In the latest revolution of the global economy, the dynamics of labour and technology in new ways as smart technological systems are built with machine learning and big data. For Vietnam, this creates major challenges as production models shift and labour no longer translates into the competitive advantage it once did.

Recognizing the importance of using available resources in the current “Fourth Industrial Revolution,” Vietnam’s government and legislature have actively pushed new policies and programmes to increase competitiveness. Resolution 52, signed by previous Communist Party General Secretary and President Nguyen Phu Trong in September 2019, outlines proactive policies to guide the country’s participation in the current economic transformation. In the resolution, the Communist Party of Vietnam pledged its commitment to a long-term strategy that would be rolled out quickly for both the political system and the society as a whole. There is also a need to increase the public’s awareness of the meaning of the Fourth Industrial Revolution, in order to make full use of new opportunities.

Vietnam is also seeking to capitalize on the country’s growing startup ecosystem. Since 2017, startup firms such as VNPay, Tiki and VNG have shown the country’s potential as a startup hub. The growing sector is driven by rising consumer spending, increasing digital revenues from e-commerce and fintech, and Vietnam’s increasing prominence as a destination for foreign investment funds.

Indonesia to Drive Digital Bank Growth

According to the World Bank, an estimated 95 million Indonesians, one-third of the country’s population, do not hold bank accounts. However, of that 95 million, 60 million own a mobile phone, representing a largely untapped market and a key avenue to offer financial services to new populations.

Digitizing payments in the private sector alone could increase bank account ownership by 29%. Many Indonesians living in rural areas live far from the nearest physical bank or ATM and have to travel significant distances to withdraw cash for payments for utilities, hospital bills, school tuition and other expenses. Digital banking would enable easier payments and give rural Indonesians access to more financial services.

Bank Jago, like a number of other fintech firms, will help increase financial services equity in the country by eradicating barriers such as geography and providing people with greater access to and ownership over their finances. Bank Jago’s move comes amid news that Indonesia’s financial services authority will now allow customers to open bank accounts and apply for loans through Gojek’s app.

3 Ways Singapore's Urban Farms are Improving Food Security

- Singapore is aiming to produce 30% of its own food by 2030, a number that is currently closer to 10%.

- To achieve this, emphasis has been put on citizens to help grow what they can.

- Growing food in urban farms on carpark rooftops to reused outdoor spaces and retrofitted building interiors is also key to the '30 by 30' goal.

Securing food during a crisis and preserving land for a livable climate is changing the focus of farming from rural areas to cities. At the forefront of this shift is Singapore, a city-sized country that aims to produce 30% of its own food by 2030. But with 90% of Singapore’s food coming from abroad, the challenge is a tall order. The plan calls for everyone in the city to grow what they can, with government grants going to those who can use technology to yield greater amounts.

The food items with potential for increased domestic production include vegetables, eggs, and fish. According to the Singapore Food Agency, these three types of goods are commonly consumed but are perishable and more susceptible to supply disruptions. Alternative proteins such as plant-based and lab-grown meats could also contribute to the “30 by 30” goal. In 2020, there were 238 licensed farms in Singapore.

KPMG Survey of Sustainability Reporting

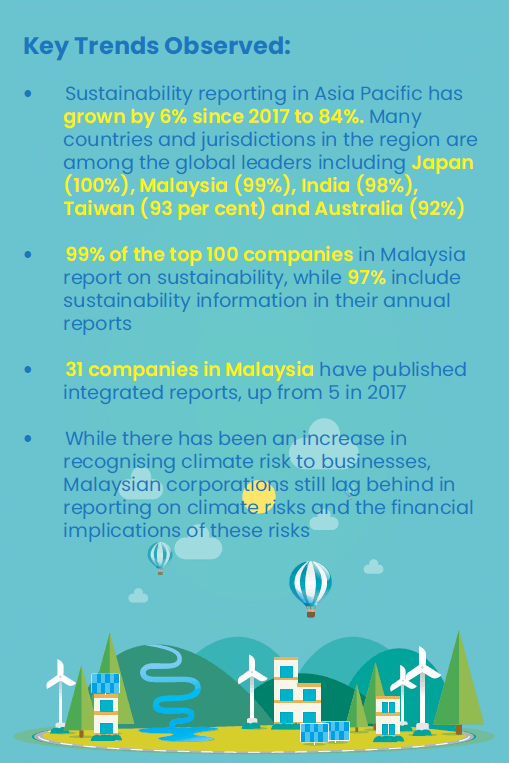

Since the survey was first published in 1993, it has tracked monumental changes in sustainability reporting. 30 years ago, a paltry 12% of companies published sustainability reports. Today, the figure stands at 80% and over 90% among the largest companies in the world. In the 11th edition of the survey, KPMG professionals reviewed sustainability reporting from 5,200 companies in 52 countries and jurisdictions – including Malaysia – making this the most extensive survey in the series to date.

CapBay Secures USD20 Million Series A Fundraising with Returning Backer KK Fund

CapBay, a fast-growing Malaysian Multi-Bank Supply Chain Finance and Peer-to-Peer Financing (“P2P”) platform, has raised US$ 20 million in its Series A round. The funding comes from returning backer KK Fund, a Singapore-based venture capital firm that invests in startups across Southeast Asia with a strong foothold in Malaysia since 2015. The Malaysian investors include several angel investors with expertise in finance, technology and growing startup companies.

CapBay aims to use the funds to further strengthen its strong technological and funding capabilities. This will enable more efficient financing and market expansion in order to reach a wide range of investors and underserved Small and medium-sized enterprises (SMEs). CapBay’s impressive business performance has laid the foundation for successful fundraising.

In December 2020, CapBay achieved a key milestone by funding RM 100 million across 500 investment notes on its P2P platform since its launch in March 2020, being the fastest fintech to hit RM100 million in P2P financing. This achievement is part of CapBay Group’s strong track record of providing supply chain finance, having facilitated more than RM 800 million across 10,000 transactions covering SMEs.

The company also expanded investment opportunities for P2P Investors on its platform through its strategic partnerships with top institutions. CapBay became the first and only fintech company selected to be part of national telecommunications giant Telekom Malaysia Bhd’s (TM) Vendor Financing Programme known as PERINTIS in September 2020. The strategic partnerships between top institutions and CapBay allowed P2P investors to invest alongside institutional investors in a safer asset class backed by the government and corporate receivables.

Recently, CapBay entered a joint venture with Kenanga to create Malaysia’s first Islamic Supply Chain Finance fintech. CapBay invests in developing the Shariah-compliant supply chain finance market through the Kenanga Capital Islamic Sdn Bhd (“KCI”) acquisition. Ang Xing Xian was appointed as CEO of KCI to grow the business and integrate with CapBay’s award-winning technology.